EUR Credit and PAB: A Match Made in Heaven?

Share

Bonds are Back and Aligned with a Greener Future

- Fixed income is back in the picture and, in our view, one of the most compelling opportunities lies within Euro-denominated investment-grade credit, which is offering yields above 4%1 with limited volatility

- Investors looking to tap into this opportunity, and also respond to the climate emergency, should consider adding a PAB tilt to their exposure

- Climate-aligned ETFs can provide cost-efficient and diversified exposure to Euro-denominated investment-grade credit aligned with the Paris Agreement, in a single transaction

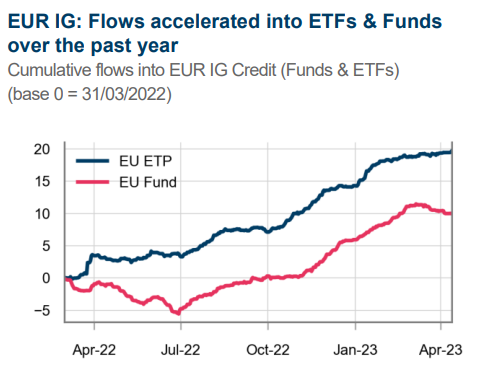

Significant flows into Corporate Bonds, confirming that “Bonds are Back”

Bonds are most definitely back in the picture and of the current fixed income opportunities available, we believe Euro-denominated investment-grade credit offers one of the most compelling risk/reward profiles.

Flows to this asset class have accelerated over the past few months (€5.7 billion YTD), supported by the positive performance of underlying exposures1. Spreads have also reverted to the levels seen at the end of Q1 2022, prior to the bond market sell-off.

Sources: Amundi ETF, Morningstar, data as at 14/04/2023.

Past performance is not a reliable indicator of future returns.

Fundamentals appear strong

Across Europe, the effects of higher policy rates are still feeding through to borrowing costs for businesses and households, and have already led to an erosion in lending and demand. Despite this, the impact on corporate credit, thus far, has been contained owing to limited refinancing needs and the high use of cash reserves built up over the Covid period. As the effects of higher rates continue to wend their way through the economy, though, a further deterioration in activity seems inevitable and we anticipate anaemic growth in Europe for this year and next.

That said, we believe that spread levels in the European corporate bond market have priced in a far bleaker-than-materialised outcome. Moreover, following last year’s sell-off, and a decade of low-to-negative interest rates, investment-grade corporate credit is exhibiting attractive valuations with yield levels comfortably above 4%1. Investment-grade credit companies will be more likely to withstand a tougher environment ahead owing to strong fundamentals. Many have even been able to increase their profit margins in the face of increased production costs.

Even in the face of the recent market turmoil, investment-grade credit quality has continued to improve with rating upgrades for EUR corporates beating downgrades for a fifth consecutive quarter.

This is in contrast to EUR high yield corporates universe where the ratio of corporate upgrades to downgrades reached its lowest level in Q1 2023 since 2020. In our view, generally higher funding costs, sluggish growth and labour costs should result in higher default rates in the high yield debt space, which we anticipate rising closer to 4% by the end of the year.

Marrying Fixed Income with the Paris Agreement

With climate change widely recognised as a clear and present threat to the planet, ever more investors are seeking to align their portfolios with the net zero goals of the Paris agreement.

So how can investors tap into the potential opportunity in Euro-denominated investment-grade credit, while responding to the climate emergency?

An increasingly popular route is via climate-aligned indices, which help investors to meet their climate objectives by tilting exposures towards constituents with better climate profiles.

Tracking Climate Aligned Benchmarks – the background

In 2019, the European Commission unveiled two benchmarks that comply with the Paris Agreement – supporting the transition to a Net-Zero world by 2050 and limiting a global average temperature rise of 1.5°C; the Climate Transition Benchmark (CTB) and the Paris-aligned Benchmark (PAB). Major index providers, quick to recognise the opportunity, responded by launching a range of climate indices complying with these benchmarks’ requirements.

Both CTB and PAB focus on a decarbonisation level of at least 7% on average per year, but PAB indices aim to reduce carbon intensity by 50%, compared to the initial investment universe, versus 30% for CTB indices. PAB indices also apply some exclusion filters on companies involved in fossil fuel exploration and coal.

PAB is thus slightly stricter with regards to its thresholds, and may therefore be more suitable for investors who want to be at the forefront of the energy transition.

Both benchmarks have been widely embraced by the sustainable finance community, and a growing number of asset managers and asset owners are incorporating PAB into their investment strategies.

Looking ahead, it’s worth considering the potential consequences of the ECB’s decision to account for climate change in its monetary policy operations by skewing future corporate bond purchases towards companies that emit less carbon. Though the ECB will only select eligible bonds, redemptions could prove greater in sectors perceived as negatively affecting climate change to the benefit of greener alternatives.

Investment-grade credit and the net zero trajectory: Capturing the opportunity

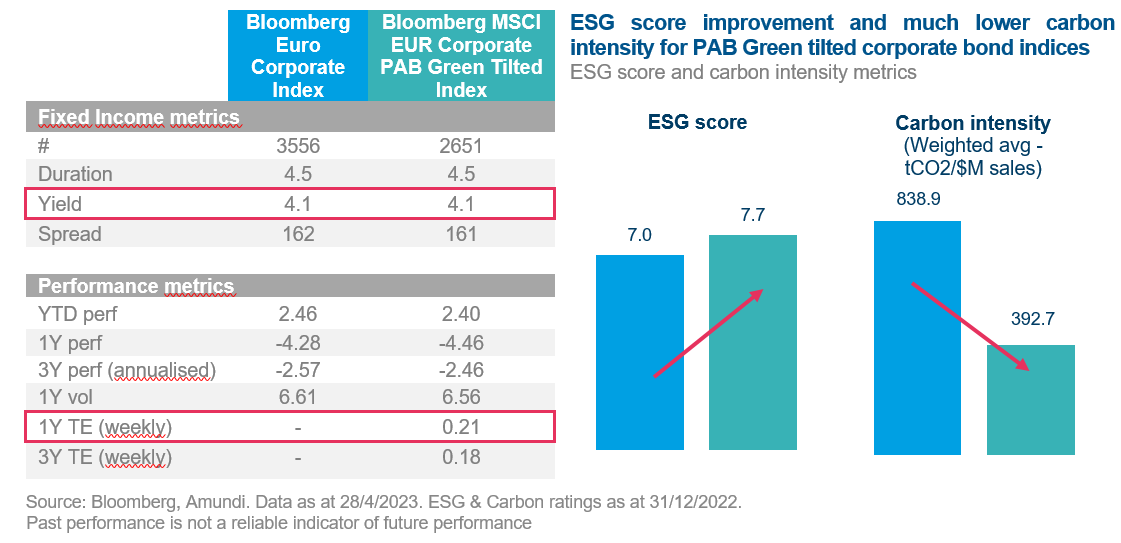

Combining investment-grade credit with a PAB benchmark can bridge the gap between having a core credit allocation with solid fundamentals and an enhanced ESG profile: the Bloomberg MSCI EUR Corporate PAB Green Tilted Index ties it all in.

The table below shows the very limited tracking error between a PAB titled corporate bond index compared to an unfiltered investment universe. At the same time, the PAB corporate bond index allows for an improved ESG score and much lower carbon intensity. Performance is also broadly comparable.

Conclusion

Bonds are offering attractive yields once again, and in our view, the case for Euro-denominated Investment Grade Credit is currently compelling. Investors wishing to tap into this opportunity, but also respond to the climate emergency may wish to consider using a PAB approach. PAB indices help investors to implement net-zero strategies in their portfolios by tilting exposures towards constituents with better climate profiles. This can result in improved ESG scores and a far lower carbon intensity without affecting performance. By investing in ETFs aligned to a PAB benchmark, investors can be assured that their investments are benchmarked against a standard that aligns with the Paris Agreement's goals.

ETF implementation idea for consideration

AMUNDI EUR CORPORATE BOND CLIMATE NET ZERO AMBITION PAB UCITS ETF ACC

Management fees: 0.14%*

*Management fees refer to the management fees and other administrative or operating costs of the fund. For more information about all the costs of investing in the fund, please refer to its Key Information Document (KID).

1. Sources: Amundi ETF, Bloomberg, data as at 17/04/2023. Past performance is not a reliable indicator of future returns

Information on Amundi’s responsible investing can be found on amundietf.com and amundi.com. The investment decision must take into account all the characteristics and objectives of the Fund, as described in the relevant Prospectus

Knowing your risk

It is important for potential investors to evaluate the risks described below and in the fund’s Key Investor Document (“KID”) or Key Investor Information Document (“KIID”) for UK investors and prospectus available on our website www.amundietf.com.

CAPITAL AT RISK - ETFs are tracking instruments. Their risk profile is similar to a direct investment in the underlying index. Investors’ capital is fully at risk and investors may not get back the amount originally invested.

UNDERLYING RISK - The underlying index of an ETF may be complex and volatile. For example, ETFs exposed to Emerging Markets carry a greater risk of potential loss than investment in Developed Markets as they are exposed to a wide range of unpredictable Emerging Market risks.

REPLICATION RISK - The fund’s objectives might not be reached due to unexpected events on the underlying markets which will impact the index calculation and the efficient fund replication.

COUNTERPARTY RISK - Investors are exposed to risks resulting from the use of an OTC swap (over-the-counter) or securities lending with the respective counterparty(-ies). Counterparty(-ies) are credit institution(s) whose name(s) can be found on the fund’s website amundietf.com. In line with the UCITS guidelines, the exposure to the counterparty cannot exceed 10% of the total assets of the fund.

CURRENCY RISK – An ETF may be exposed to currency risk if the ETF is denominated in a currency different to that of the underlying index securities it is tracking. This means that exchange rate fluctuations could have a negative or positive effect on returns.

LIQUIDITY RISK – There is a risk associated with the markets to which the ETF is exposed. The price and the value of investments are linked to the liquidity risk of the underlying index components. Investments can go up or down. In addition, on the secondary market liquidity is provided by registered market makers on the respective stock exchange where the ETF is listed. On exchange, liquidity may be limited as a result of a suspension in the underlying market represented by the underlying index tracked by the ETF; a failure in the systems of one of the relevant stock exchanges, or other market-maker systems; or an abnormal trading situation or event.

VOLATILITY RISK – The ETF is exposed to changes in the volatility patterns of the underlying index relevant markets. The ETF value can change rapidly and unpredictably, and potentially move in a large magnitude, up or down.

CONCENTRATION RISK – Thematic ETFs select stocks or bonds for their portfolio from the original benchmark index. Where selection rules are extensive, it can lead to a more concentrated portfolio where risk is spread over fewer stocks than the original benchmark.

Important information

This material is solely for the attention of professional and eligible counterparties, as defined in Directive MIF 2014/65/UE of the European Parliament acting solely and exclusively on their own account. It is not directed at retail clients. In Switzerland, it is solely for the attention of qualified investors within the meaning of Article 10 paragraph 3 a), b), c) and d) of the Federal Act on Collective Investment Scheme of June 23, 2006.

This information is not for distribution and does not constitute an offer to sell or the solicitation of any offer to buy any securities or services in the United States or in any of its territories or possessions subject to its jurisdiction to or for the benefit of any U.S. Person (as defined in the prospectus of the Funds or in the legal mentions section on www.amundi.com and www.amundietf.com. The Funds have not been registered in the United States under the Investment Company Act of 1940 and units/shares of the Funds are not registered in the United States under the Securities Act of 1933.

This material reflects the views and opinions of the individual authors at this date and in no way the official position or advices of any kind of these authors or of Amundi Asset Management nor any of its subsidiaries and thus does not engage the responsibility of Amundi Asset Management nor any of its subsidiaries nor of any of its officers or employees. This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It is explicitly stated that this document has not been prepared by reference to the regulatory requirements that seek to promote independent financial analysis. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Neither Amundi Asset Management nor any of its subsidiaries accept liability, whether direct or indirect, that may result from using any information contained in this document or from any decision taken the basis of the information contained in this document. Clients should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, if appropriate, seek professional advice, including tax advice. Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients and principal trading desks that reflect opinions that are contrary to the opinions expressed in this research. Our asset management area, principal trading desks and investing businesses may make investment decisions that are inconsistent with the recommendations or views expressed in this research.

This document is of a commercial nature. The funds described in this document (the “Funds”) may not be available to all investors and may not be registered for public distribution with the relevant authorities in all countries. It is each investor’s responsibility to ascertain that they are authorised to subscribe, or invest into this product. Prior to investing in the product, investors should seek independent financial, tax, accounting and legal advice.

This is a promotional and non-contractual information which should not be regarded as an investment advice or an investment recommendation, a solicitation of an investment, an offer or a purchase, from Amundi Asset Management (“Amundi”) nor any of its subsidiaries.

The Funds are Amundi UCITS ETFs. The Funds can either be denominated as “Amundi ETF” or “Lyxor ETF”. Amundi ETF designates the ETF business of Amundi.

The Funds are French, Luxembourg open ended mutual investment funds respectively approved by the French Autorité des Marchés Financiers, the Luxembourg Commission de Surveillance du Secteur Financier, and authorised for marketing of their units or shares in various European countries (the Marketing Countries) pursuant to the article 93 of the 2009/65/EC Directive.

Amundi UCITS ETFs are passively-managed index-tracking funds. The Funds can be French Fonds Communs de Placement (FCPs) and also be sub-funds of the following umbrella structures:

For Amundi ETF:

- Amundi Index Solutions, Luxembourg SICAV, RCS B206810, located 5, allée Scheffer, L-2520, managed by Amundi Luxembourg S.A.

For Lyxor ETF:

- Multi Units France, French SICAV, RCS 441 298 163, located 91-93, boulevard Pasteur, 75015 Paris, France, managed by Amundi Asset Management

- Multi Units Luxembourg, RCS B115129 and Lyxor Index Fund, RCS B117500, both Luxembourg SICAV located 9, rue de Bitbourg, L-1273 Luxembourg, and managed by Amundi Asset Management

- Lyxor SICAV, Luxembourg SICAV, RCS B140772, located 5, Allée Scheffer, L-2520 Luxembourg, managed by Amundi Luxembourg S.A.

Before any subscriptions, the potential investor must read the offering documents (KID or KIID for UK investors and prospectus) of the Funds. The prospectus in French for French UCITS ETFs, and in English for Luxembourg UCITS ETFs, and the KID or KIID for UK investors in the local languages of the Marketing Countries are available free of charge on www.amundi.com, www.amundi.ie or www.amundietf.com. They are also available from the headquarters of Amundi Luxembourg S.A. (as the management company of Amundi Index Solutions and Lyxor SICAV), or the headquarters of Amundi Asset Management (as the management company of Amundi ETF French FCPs, Multi Units Luxembourg, Multi Units France and Lyxor Index Fund).

Investment in a fund carries a substantial degree of risk (i.e. risks are detailed in the KID or KIID for UK investors and prospectus). Past Performance does not predict future returns. Investment return and the principal value of an investment in funds or other investment product may go up or down and may result in the loss of the amount originally invested. All investors should seek professional advice prior to any investment decision, in order to determine the risks associated with the investment and its suitability.

It is the investor’s responsibility to make sure his/her investment is in compliance with the applicable laws she/he depends on, and to check if this investment is matching his/her investment objective with his/her patrimonial situation (including tax aspects).

Please note that the management companies of the Funds may de-notify arrangements made for marketing as regards units/shares of the Fund in a Member State of the EU in respect of which it has made a notification.

A summary of information about investors’ rights and collective redress mechanisms can be found in English on the regulatory page at https://about.amundi.com/Metanav-Footer/Footer/Quick-Links/Legal-documentation with respect to Amundi ETFs.

This document was not reviewed, stamped or approved by any financial authority.

This document is not intended for and no reliance can be placed on this document by persons falling outside of these categories in the below mentioned jurisdictions. In jurisdictions other than those specified below, this document is for the sole use of the professional clients and intermediaries to whom it is addressed. It is not to be distributed to the public or to other third parties and the use of the information provided by anyone other than the addressee is not authorised.

This material is based on sources that Amundi and/or any of her subsidiaries consider to be reliable at the time of publication. Data, opinions and analysis may be changed without notice. Amundi and/or any of her subsidiaries accept no liability whatsoever, whether direct or indirect, that may arise from the use of information contained in this material. Amundi and/or any of her subsidiaries can in no way be held responsible for any decision or investment made on the basis of information contained in this material.

Updated composition of the product’s investment portfolio is available on www.amundietf.com. Units of a specific UCITS ETF managed by an asset manager and purchased on the secondary market cannot usually be sold directly back to the asset manager itself. Investors must buy and sell units on a secondary market with the assistance of an intermediary (e.g. a stockbroker) and may incur fees for doing so. In addition, investors may pay more than the current net asset value when buying units and may receive less than the current net asset value when selling them.

Indices and the related trademarks used in this document are the intellectual property of index sponsors and/or its licensors. The indices are used under license from index sponsors. The Funds based on the indices are in no way sponsored, endorsed, sold or promoted by index sponsors and/or its licensors and neither index sponsors nor its licensors shall have any liability with respect thereto. The indices referred to herein (the “Index” or the “Indices”) are neither sponsored, approved or sold by Amundi nor any of its subsidiaries. Neither Amundi nor any of its subsidiaries shall assume any responsibility in this respect.

Information reputed exact as of the date mentioned above.

Reproduction prohibited without the written consent of Amundi.