Mid-year Outlook 2026:

ETF Implementation Ideas

Power of endurance: staying invested, staying selective

Jump to key sections

Views are those of Amundi as of 10/07/2026 and are subject to change.

Power of endurance: staying invested, staying selective

The Amundi Investment Institute's mid-year outlook carries a clear message: this is not a standard late-cycle environment, and it may not reward standard late-cycle portfolios.

The energy supply shock which has defined the first half of 2026 has pushed inflation higher, hamstrung central banks and forced a meaningful reassessment of where growth and risk sit.

This is why we believe investors1 may consider portfolios that can withstand different scenarios while remaining invested in genuine structural opportunities.

We see the macro backdrop for H2 2026 is one of uneven resilience. The US is expected to grow at around 2%,2 supported by AI-driven capital expenditure, even as household demand softens. The eurozone, having borne the brunt of the energy shock, faces a more difficult path, and we expect the ECB to deliver one further precautionary rate hike before the year is out. Emerging markets (EM) continue to outpace developed markets (DM) as a whole, though with significant divergence within the bloc.3

Against this backdrop, we set out our ETF implementation ideas for six key investment themes1 for the second half of the year.

Seek breadth, avoid concentration

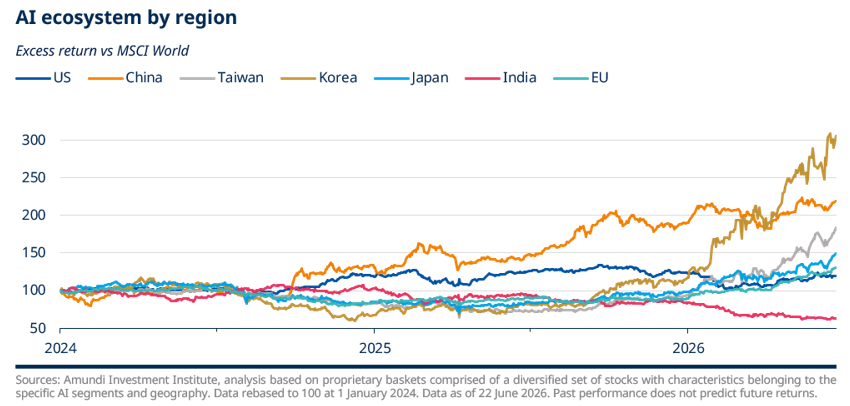

Artificial Intelligence (AI) remains a structural equity driver, but avoiding concentration risk will be key. Look to a broader opportunity set from infra providers to AI adopters across sectors and regions.

While among the most powerful structural drivers in global equity markets, AI’s value is increasingly spread across infrastructure, hardware and adoption. The question for H2 2026 may no longer be who can build the next frontier, but who can scale it.

We believe there are opportunities across four segments: upstream (semiconductor manufacturing, chips, hardware), upstream/midstream (memory, packaging, server and network infrastructure), midstream (data centres, cloud, AI deployment) and downstream (end-user applications and platforms). Upstream segments have driven the strongest performance to date,4 but the opportunity is now widening into deployment and adoption - and critically, it is spreading geographically.

China – supported by industrial capacity, state backing, energy access, and bargaining power in critical materials – is strong in AI deployment and industrial scaling, while South Korea dominates AI memory through high-bandwidth memory chips. Taiwan is central to foundry and advanced packaging – two of AI's most important hardware bottlenecks – while Europe is capturing value as an AI infrastructure, industrial and regulated adoption enabler.

Given the broad opportunity set, investors seeking a resilient way to benefit from AI could consider thematic and sector exposures to capture the breadth of the value chain.

We remain selective on US equities and favour exposures beyond highly valued mega caps, therefore investors could refocus allocation through equal-weight strategies or US ex-mega cap exposures1 in order to mitigate concentration risk.9

ETF implementation ideas

For more information regarding the investment objectives of the fund, please refer to the Key Information Documents (KID) and the prospectus.

Invest in Europe's capex revival

Europe’s strategic autonomy agenda is becoming a multi-year investment cycle across defence, energy security, AI infrastructure and industrial renewal.

Europe is entering a new growth regime as it transitions from a consumption-led economy to a multi-year investment story. As resilience, sovereignty and competitiveness come to the fore, there is a clear reallocation of capital toward energy security, defence, technological sovereignty and infrastructure renewal.

The scale of the investment is transformative. European industrial capex grew 182% in 2024–25 versus the 2010–19 average, while German fiscal spending – largely on defence and infrastructure – is forecast to boost GDP growth by 0.8% in 2026.5

With this in mind, defence and security remain multi-year growth themes. In defence, the procurement cycle has barely begun, leaving significant runway for investment as European countries rebuild capabilities and stockpiles.

Meanwhile the transition toward electrification requires major investment in power grids, transmission, storage, among other infrastructure aspects. Europe’s rising electricity demand and ageing infrastructure create a supportive long-duration capex cycle.

Additionally, the region’s efforts to reduce dependence on foreign suppliers and rebuild industrial capacity is supportive of construction, engineering, capital goods, industrial automation and infrastructure services – underpinned by growing AI power demand.

European healthcare companies stand to benefit both from AI-driven efficiency gains in drug development and diagnostics, and from Europe's push to build greater pharmaceutical and medical supply chain sovereignty being pushed by the strategic autonomy theme.

As such, investors1 could explore European equity exposures that may capture the potential winners of the build-out of European strategic capacity.

ETF implementation ideas

For more information regarding the investment objectives of the fund, please refer to the Key Information Documents (KID) and the prospectus.

Adjust to the yield reset

Higher yields have made bonds more appealing, but with debt high and policy paths unclear, flexibility is key to capturing bond income.

Higher yields mean fixed income could once again offer a more meaningful income potential to portfolios than at any point in the post-financial crisis era.3 But navigating bond markets in H2 2026 may require considerably more precision than simply adding duration.

We anticipate the ECB to deliver one further hike in 2026, without embarking on a full tightening cycle, potentially making short-dated EUR bonds attractive, as markets may be pricing in too much tightening.

In the US, the Fed remains on hold, constrained by inflation persistently above 3% and uncertainty around central bank independence under the new Fed Chair. We are therefore neutral on US duration and suggest investors1 explore opportunities elsewhere.

In our view, the biggest pocket of opportunity could be in European investment-grade credit, which despite strong fundamentals offers better value relative to US investment grade, and should tighten in the medium term.

We believe there is a strong case for a range of duration exposures. Floating rate instruments can provide a natural buffer against policy tightening, while ultra-short and short-dated bonds look to offer income with limited rate sensitivity. Overnight return strategies aim to offer an efficient cash management option, especially at a time when short-term European rates are at elevated levels. They could generate a potential meaningful return, making them a practical tool for investors seeking to position cash defensively in times of uncertainty.

ETF implementation ideas

For more information regarding the investment objectives of the fund, please refer to the Key Information Documents (KID) and the prospectus.

Diverging opportunities across emerging markets

Favour countries that are supply-chain winners, commodity exporters, or those with credible policy frameworks. Be cautious where dollar sensitivity is high and external balances are weak.

Not all emerging markets are equal and thus, for investors, precision has never mattered more.

EMs overall continue to offer a meaningful growth premium over developed markets. China’s GDP is forecast to grow at 4.5% in 2026 and India’s at 6.6%, comfortably ahead of the US at 2.0% and the eurozone at 0.5%.7 A weaker US dollar provides a further structural tailwind for the asset class.

However, the aggregate growth number conceals a wide dispersion of outcomes.

Investors1 should favour countries that are supply-chain winners, commodity exporters, or those with credible policy frameworks. They should be cautious on countries with high dollar sensitivity and weak external balances.

Within Asia, South Korea and Taiwan have been among the strongest contributors to EM equity performance year-to-date,4 driven by their central roles in the AI hardware value chain, such as memory chips and semiconductors.

China A-shares can offer a more targeted route into China's domestic AI and technology opportunity. With A-shares representing approximately 20% of MSCI China,8 a dedicated onshore allocation may capture a sector tilt that is distinctly different from the offshore index, with greater exposure to the technology and industrial themes we favour.

In Latin America, we are particularly positive on Brazil. Earnings and profitability remain high, its easing cycle is ongoing, and commodity exposure offers a potential inflation buffer.3 The region’s limited AI exposure could also add a layer of diversifying9 source of returns.

ETF implementation ideas

For more information regarding the investment objectives of the fund, please refer to the Key Information Documents (KID) and the prospectus.

Back real assets in an era of inflation

Increase focus on the real economy, real assets, commodities, and infrastructure as stores of value at a time of higher risk of value erosion from inflation.

The Amundi Investment Institute's proprietary Inflation Phazer model signals we are entering an inflationary regime, with US CPI expected to remain above 3% for the remainder of 2026.10 While it does not indicate a repeat of the 2022 shock, it can be a meaningful shift with consequences for portfolio construction.

In previous inflationary regimes, gold and commodities have significantly outperformed nominal bonds and offered competitive returns relative to equities.4 Cash has a potential to become a structural decision, and the duration component of a traditional balanced portfolio may become a less reliable diversifier9 in inflation-driven stress episodes.9

Against this backdrop, the case for diversifying9 into the real economy, commodities and infrastructure has become strong. It is also a case for geographic rebalancing. GDP-weighted strategies tend to tilt naturally to a more balanced exposure and reflect more accurately the real global economy, including Europe and emerging markets, which may be better positioned to capture the next wave of growth.

Commodities and materials can provide a direct inflation diversifier9, while also potentially benefiting from structural demand linked to AI infrastructure, the energy transition and industrial renewal.

USD floating rate credit strategies could also offer income resilience in a scenario where the Fed remains on hold at elevated rates, as they may reward investors for staying patient in a higher-for-longer interest rate environment.

ETF implementation ideas

For more information regarding the investment objectives of the fund, please refer to the Key Information Documents (KID) and the prospectus.

Rethink the traditional hedge

Higher inflation, geopolitical volatility and USD debasement are key risks. Duration alone is not enough. A broad protection toolkit includes gold and hedging strategies.

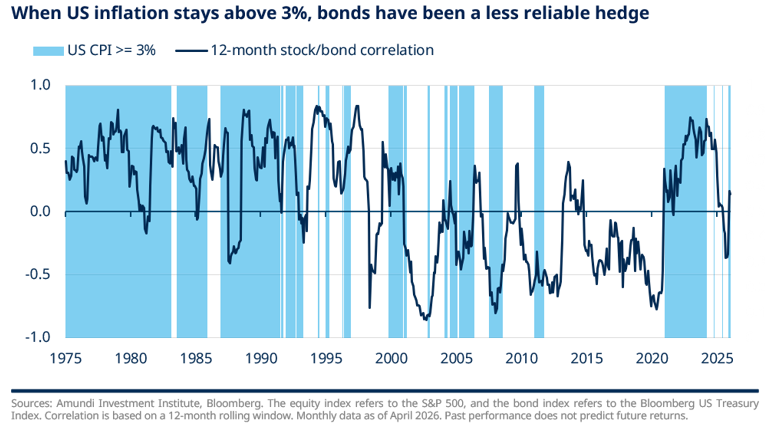

When US CPI stays above 3%, bonds have historically been a less reliable hedge, as the stock-bond correlation tends to be persistently positive.3 Duration alone therefore may not be enough, and investors should consider building a broader protection toolkit.

In H2 2026, with high debt-to-GDP levels across most developed economies, uncertainty around the Fed's institutional framework, and the risk of renewed energy price pressure, the traditional “safe-haven” playbook needs updating.

Gold remains the most common diversifier9, especially in an environment of currency debasement and geopolitical stress. Over the medium term, we remain bullish with a $5,500 price target,11 supported by strong central bank buying from emerging markets and rising global debt levels. Gold miners, on the other hand, can offer an equity expression of the same thesis.

Inflation-linked bond strategies could provide a structural buffer for real fixed income value in a persistently inflationary environment.

Meanwhile, income-focused solutions on major equity indices, such as the Euro STOXX 50 and Nasdaq-100 index, offer a potential way to remain invested in equity markets while moderating volatility through yield generation.

Implementation ideas

For more information regarding the investment objectives of the fund, please refer to the Key Information Documents (KID) and the prospectus.

To conclude: Built to endure and stay invested

The “Power of Endurance” is the capacity to stay invested through volatility, to hold conviction through uncertainty and to build portfolios that do not simply survive the current environment but aim to potentially benefit1 from its structural shifts.

The risks are real: a prolonged Strait of Hormuz disruption, AI disappointment, or a more aggressive central bank response could all challenge the base case. But the toolkit to navigate those risks exists, in thematics, in genuine geographic diversification9, in agile fixed income positioning and in a diversifying9 approach that goes beyond duration.

We believe that the push for European strategic autonomy, the broadening of the AI supercycle, and the inflationary implications of geopolitical fragmentation provide the opportunities within the investment roadmap for H2 2026 and beyond.

Amundi's ETF range provides the building blocks to act on each of these convictions with the precision and flexibility that the current environment demands.

1.Investment involves risks. For more information, please refer to the Risk section below.

2.Source: Bloomberg, Amundi Investment Institute forecasts

3.Past market trends are not a reliable indicator of future ones.

4.Past performance does not predict future returns.

5.Sources: Amundi Investment Institute, analysis on MSCI Europe Industrials index capes, and the Germany Bundesbank.

6.Sources: Amundi Investment Institute, NATO, Bloomberg Economics Forecasts. Note: Defence spending as a percentage of GDP is a weighted average. Data as of February 2026.

7.Source: Amundi Investment Institute, data as of 22 June 2026.

8.Source: MSCI, as of 30 June 2026. For more information regarding the index methodology please refer to www.msci.com.

9.Diversification does not guarantee a profit or protect against a loss.

10.Sources: Amundi Investment Institute, Bloomberg. Data as of 15 June 2026. For illustrative purposes.

11.Source: Amundi Investment Institute, as of 17 June 2026.

Marketing Communication for professional investors.

Views expressed in this communication are those of Amundi as of its publication date and are subject to change.

Information on Amundi’s responsible investing can be found on amundietf.com and amundi.com. The investment decision must take into account all the characteristics and objectives of the Fund, as described in the relevant Prospectus.

KNOWING YOUR RISKS

It is important for potential investors to evaluate the risks described below and in the fund’s Key Information Document (“KID”) and prospectus available on our websites www.amundietf.com. (click here to read the full risks)

CAPITAL AT RISK - ETFs are tracking instruments. Their risk profile is similar to a direct investment in the underlying index securities. Investors’ capital is fully at risk and investors may not get back the amount originally invested.

UNDERLYING RISK - The underlying index securities of an ETF may be complex and volatile. For example, ETFs exposed to Emerging Markets carry a greater risk of potential loss than investment in Developed Markets as they are exposed to a wide range of unpredictable Emerging Market risks.

REPLICATION RISK - The fund’s objectives might not be reached due to unexpected events on the underlying markets which will impact the index calculation and the efficient fund replication.

COUNTERPARTY RISK - Investors are exposed to risks resulting from the use of an OTC swap (over-the-counter) or securities lending with the respective counterparty(-ies). Counterparty(-ies) are credit institution(s) whose name(s) can be found on the fund’s website amundietf.com. In line with the UCITS guidelines, the exposure to the counterparty cannot exceed 10% of the total assets of the fund.

CURRENCY RISK – An ETF may be exposed to currency risk if the ETF is denominated in a currency different to that of the underlying index securities it is tracking. This means that exchange rate fluctuations could have a negative or positive effect on returns.

LIQUIDITY RISK – There is a risk associated with the markets to which the ETF is exposed. The price and the value of investments are linked to the liquidity risk of the underlying index securities. Investments can go up or down. In addition, on the secondary market liquidity is provided by registered market makers on the respective stock exchange where the ETF is listed. On exchange, liquidity may be limited as a result of a suspension in the underlying market represented by the underlying index tracked by the ETF; a failure in the systems of one of the relevant stock exchanges, or other market-maker systems; or an abnormal trading situation or event.

VOLATILITY RISK – The ETF is exposed to changes in the volatility patterns of the underlying index relevant markets. The ETF value can change rapidly and unpredictably, and potentially move in a large magnitude, up or down.

CONCENTRATION RISK – ETFs can select a large portion of their assets in a particular issuer, industry, stocks or type of bonds, country or region for their portfolio. Where selection rules are extensive, it can lead to a more concentrated portfolio where risk is spread over fewer stocks. Where selection rules are extensive, it can lead to a more concentrated portfolio where risk is spread over fewer stocks. This can mean both higher volatility and a greater risk of loss.

CREDIT WORTHINESS – The investors are exposed to the creditworthiness of the Issuer

IMPORTANT INFORMATION

This material is solely for the attention of professional and eligible counterparties, as defined in Directive MIF 2014/65/UE of the European Parliament acting solely and exclusively on their own account. It is not directed at retail clients. In Switzerland, it is solely for the attention of qualified investors within the meaning of Article 10 paragraph 3 a), b), c) and d) of the Federal Act on Collective Investment Scheme of June 23, 2006.

This material reflects the views and opinions of the individual authors at this date and in no way the official position or advices of any kind of these authors or of Amundi Asset Management nor any of its subsidiaries and thus does not engage the responsibility of Amundi Asset Management nor any of its subsidiaries nor of any of its officers or employees. This research is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. It is explicitly stated that this document has not been prepared by reference to the regulatory requirements that seek to promote independent financial analysis. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Neither Amundi Asset Management nor any of its subsidiaries accept liability, whether direct or indirect, that may result from using any information contained in this document or from any decision taken the basis of the information contained in this document.

Clients should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, if appropriate, seek professional advice, including tax advice. Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to our clients and principal trading desks that reflect opinions that are contrary to the opinions expressed in this research. Our asset management area, principal trading desks and investing businesses may make investment decisions that are inconsistent with the recommendations or views expressed in this research.

This information is not for distribution and does not constitute an offer to sell or the solicitation of any offer to buy any securities or services in the United States or in any of its territories or possessions subject to its jurisdiction to or for the benefit of any U.S. Person (as defined in the prospectus of the Funds or in the legal mentions section on www.amundi.com and www.amundietf.com. The Funds have not been registered in the United States under the Investment Company Act of 1940 and units/shares of the Funds are not registered in the United States under the Securities Act of 1933.

This document is of a commercial nature. The funds described in this document (the “Funds”) may not be available to all investors and may not be registered for public distribution with the relevant authorities in all countries. It is each investor’s responsibility to ascertain that they are authorised to subscribe, or invest into this product. Prior to investing in the product, investors should seek independent financial, tax, accounting and legal advice. This is a promotional and non-contractual information which should not be regarded as an investment advice or an investment recommendation, a solicitation of an investment, an offer or a purchase, from Amundi Asset Management (“Amundi”) nor any of its subsidiaries.

The Funds are Amundi UCITS ETFs and Amundi ETF designates the ETF business of Amundi.

Amundi UCITS ETFs are passively-managed index-tracking funds. The Funds are French, Luxembourg or Irish open ended mutual investment funds respectively approved by the French Autorité des Marchés Financiers, the Luxembourg Commission de Surveillance du Secteur Financier or the Central Bank of Ireland, and authorised for marketing of their units or shares in various European countries (the Marketing Countries) pursuant to the article 93 of the 2009/65/EC Directive.

The Funds can be French Fonds Communs de Placement (FCPs) and also be sub-funds of the following umbrella structures:

- Amundi Index Solutions, Luxembourg SICAV, RCS B206810, located 5, allée Scheffer, L-2520, managed by Amundi Luxembourg S.A.

- Amundi ETF ICAV: open-ended umbrella Irish collective asset-management vehicle established under the laws of Ireland and authorized for public distribution by the Central Bank of Ireland.

The management company of the Fund is Amundi Ireland Limited, 1 George’s Quay Plaza, George’s Quay, Dublin 2, D02 V002, Ireland.

Amundi Ireland Limited is authorised and regulated by the Central Bank of Ireland

- Multi Units France, French SICAV, RCS 441 298 163, located 91-93, boulevard Pasteur, 75015 Paris, France managed by Amundi Asset Management located 91-93, boulevard Pasteur, 75015 Paris

- Multi Units Luxembourg, RCS B115129, Luxembourg SICAV located 9, rue de Bitbourg, L-1273 Luxembourg, managed by Amundi Luxembourg S.A. located 5, allée Scheffer, L-2520 Luxembourg Before any subscriptions, the potential investor must read the offering documents (KID and prospectus) of the Funds.

The prospectus in French for French UCITS ETFs, and in English for Luxembourg UCITS ETFs and Irish UCITS ETFs, and the KID in the local languages of the Marketing Countries are available free of charge on www.amundi.com, www.amundi.ie or www.amundietf.com.

They are also available from the headquarters of Amundi Luxembourg S.A. (as the management company of Amundi Index Solutions and Multi Units Luxembourg), or the headquarters of Amundi Asset Management (as the management company of Amundi ETF French FCPs and Multi Units France), or at the headquarters of Amundi Ireland Limited (as the management company of Amundi ETF ICAV). For more information related to the stocks exchanges where the ETF is listed please refer to the fund’s webpage on amundietf.com.

Investment in a fund carries a substantial degree of risk (i.e. risks are detailed in the KID and prospectus). Past Performance does not predict future returns. Investment return and the principal value of an investment in funds or other investment product may go up or down and may result in the loss of the amount originally invested.

All investors should seek professional advice prior to any investment decision, in order to determine the risks associated with the investment and its suitability. It is the investor’s responsibility to make sure his/her investment is in compliance with the applicable laws she/he depends on, and to check if this investment is matching his/her investment objective with his/her patrimonial situation (including tax aspects). Please note that the management companies of the Funds may de-notify arrangements made for marketing as regards units/shares of the Fund in a Member State of the EU or the UK in respect of which it has made a notification.

A summary of information about investors’ rights and collective redress mechanisms can be found in English on the regulatory page at https://about.amundi.com/legal-documentation with respect to Amundi ETFs.

This document was not reviewed, stamped or approved by any financial authority. This document is not intended for and no reliance can be placed on this document by persons falling outside of these categories in the below mentioned jurisdictions. In jurisdictions other than those specified below, this document is for the sole use of the professional clients and intermediaries to whom it is addressed. It is not to be distributed to the public or to other third parties and the use of the information provided by anyone other than the addressee is not authorised.

This material is based on sources that Amundi and/or any of her subsidiaries consider to be reliable at the time of publication. Data, opinions and analysis may be changed without notice. Amundi and/or any of her subsidiaries accept no liability whatsoever, whether direct or indirect, that may arise from the use of information contained in this material. Amundi and/or any of her subsidiaries can in no way be held responsible for any decision or investment made on the basis of information contained in this material. Updated composition of the product’s investment portfolio is available on www.amundietf.com.

Units of a specific UCITS ETF managed by an asset manager and purchased on the secondary market cannot usually be sold directly back to the asset manager itself. Investors must buy and sell units on a secondary market with the assistance of an intermediary (e.g. a stockbroker) and may incur fees for doing so. In addition, investors may pay more than the current net asset value when buying units and may receive less than the current net asset value when selling them. Indices and the related trademarks used in this document are the intellectual property of index sponsors and/or its licensors.

The indices are used under license from index sponsors. The Funds based on the indices are in no way sponsored, endorsed, sold or promoted by index sponsors and/or its licensors and neither index sponsors nor its licensors shall have any liability with respect thereto.

The indices referred to herein (the “Index” or the “Indices”) are neither sponsored, approved or sold by Amundi nor any of its subsidiaries. Neither Amundi nor any of its subsidiaries shall assume any responsibility in this respect.

AMUNDI PHYSICAL GOLD ETC (the “ETC”) is a series of debt securities governed by Irish Law and issued by Amundi Physical Metals plc, a dedicated Irish vehicle (the “Issuer”). The Base Prospectus, and supplement to the Base Prospectus, of the ETC has been approved by the Central Bank of Ireland (the “Central Bank”), as competent authority under the Prospectus Directive. Pursuant to the Directive Prospective Regulation, the ETC is described in a Key Information Document (KID), final terms and Base Prospectus (hereafter the Legal Documentation). The ETC KID must be made available to potential subscribers prior to subscription. The Legal Documentation can be obtained from Amundi on request. The distribution of this document and the offering or sale of the ETC Securities in certain jurisdictions may be restricted by law. For a description of certain restrictions on the distribution of this document, please refer to the Base Prospectus.

The investors are exposed to the creditworthiness of the Issuer. In EEA Member States, the content of this document is approved by Amundi for use with Professional Clients (as defined in EU Directive 2004/39/EC) only and shall not be distributed to the public.

Information reputed exact as of 10/07/2026. Reproduction prohibited without the written consent of Amundi.